If you’ve ever wondered why your credit score isn’t improving even when you pay your bills on time your credit utilization ratio might be the hidden reason.

Most people focus only on payments, but lenders look at something deeper: how much of your available credit you’re actually using.

This single factor can make or break your credit profile.

In this guide, you’ll learn everything you need to know about credit utilization, including real examples, expert tips, and simple strategies to keep your ratio low and your score rising.

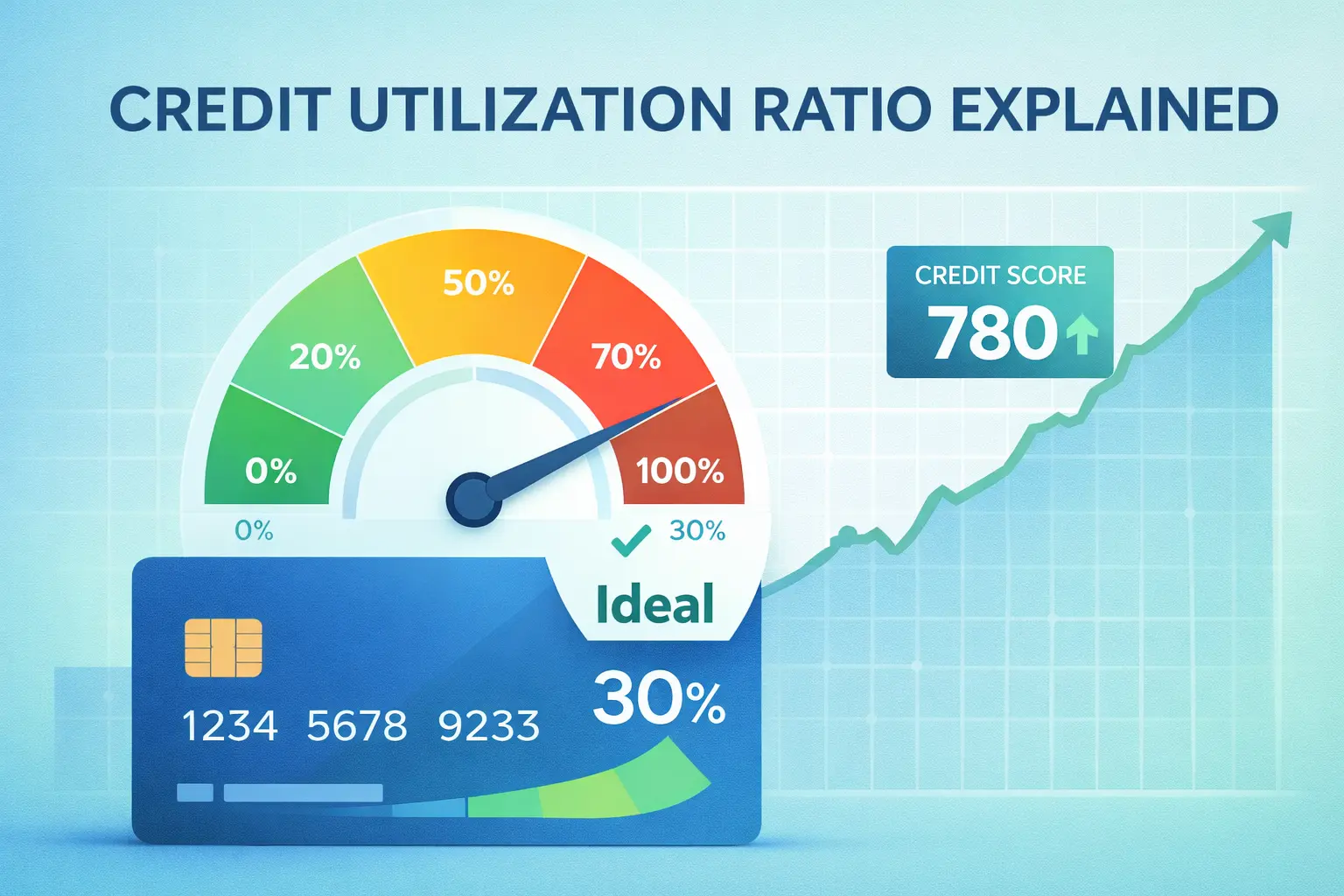

What Is Credit Utilization Ratio?

At its core, the credit utilization ratio measures how much of your available credit you’re currently using.

It’s expressed as a percentage and applies to both:

- Individual credit cards

- Your total credit across all accounts

Simple Formula:

Credit Utilization = (Credit Balance ÷ Credit Limit) × 100

Let’s make this easy to understand:

- If your credit limit is $10,000

- And your total balance is $3,000

Your utilization ratio is 30%

That means you’re using 30% of the credit available to you.

Choosing the best cashback credit cards 2026 can help you manage your spending efficiently.

Table of Contents for Credit Utilization Ratio Explained

Why Credit Utilization Matters for Your Credit Score

Your credit utilization is one of the most powerful factors in determining your credit score.

It accounts for roughly 30% of your total score, making it second only to payment history.

Lenders and scoring models—based on systems described under Credit score—use this ratio to evaluate how risky you are as a borrower.

Here’s how they interpret it:

- Low utilization → You’re responsible and not dependent on credit

- High utilization → You might be overextended financially

Even if you never miss a payment, high utilization can still lower your score significantly.

This is why understanding it is essential in Personal finance.

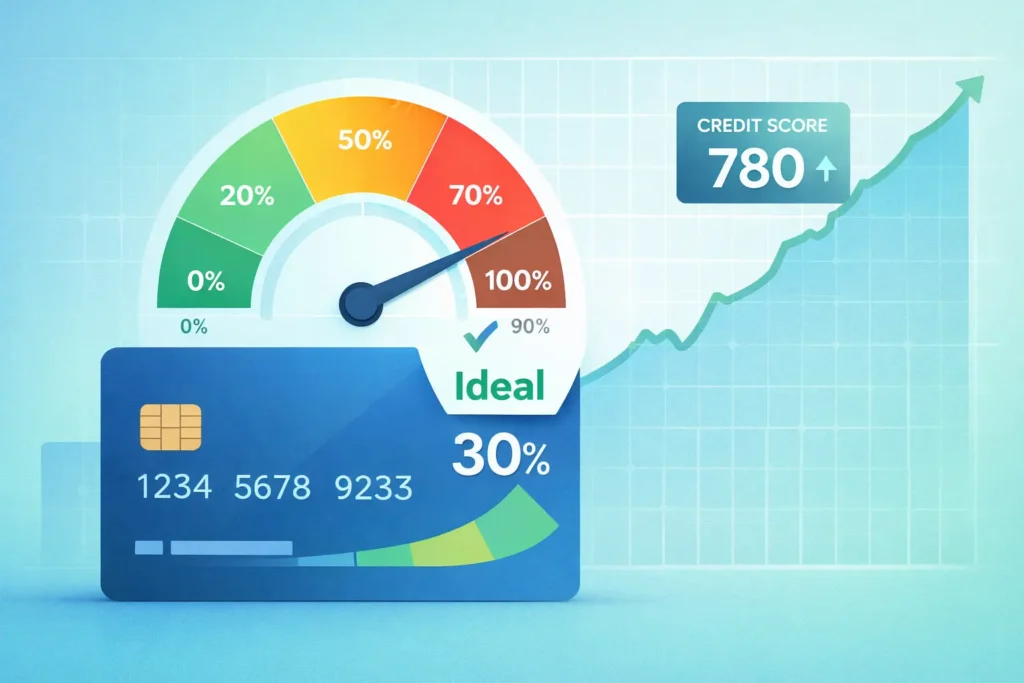

What Is a Good Credit Utilization Ratio?

Not all utilization levels are treated equally. Here’s a practical breakdown:

- 0%–10% → Excellent (best for top-tier scores)

- 10%–30% → Good (safe and recommended)

- 30%–50% → Risky (may lower your score)

- Above 50% → Poor (high credit risk signal)

Key Rule:

Always aim to keep your credit utilization below 30%

But if you really want excellent credit, try staying under 10%.

Does Credit Utilization Matter If You Pay in Full?

This is one of the most misunderstood topics.

Many people believe that if they pay their credit card balance in full every month, utilization doesn’t matter.

That’s not true.

Your utilization is calculated based on your statement balance, not your payment.

Here’s what happens:

- You spend $2,000 on a card with a $3,000 limit

- Your statement closes → utilization is 66%

- You pay it off in full afterward

👉 Your credit report still shows 66% utilization

That can temporarily lower your score—even though you’re financially responsible.

How Much Will Lowering Credit Utilization Affect Your Score?

Reducing your utilization is one of the fastest ways to improve your credit score.

In many cases, you can see results within a few weeks to one billing cycle.

Real Impact Examples:

- Reducing from 80% → 30%

→ Significant score increase - Reducing from 30% → 10%

→ Moderate improvement - Reducing from 10% → 5%

→ Smaller but still valuable gain

The higher your starting utilization, the bigger the impact when you lower it.

Before improving utilization, it’s helpful to know what is a good credit score in USA.

Credit Utilization Ratio Example (Real Numbers)

Let’s walk through a realistic scenario to make this crystal clear.

Example 1: High Utilization

- Credit limit: $5,000

- Balance: $4,000

- Utilization: 80%

This signals high risk and can lower your score.

Example 2: متوسط (Average)

- Credit limit: $5,000

- Balance: $1,500

- Utilization: 30%

This is acceptable but not ideal.

Example 3: Low Utilization

- Credit limit: $5,000

- Balance: $500

- Utilization: 10%

This is where you want to be for strong credit health.

How to Keep Credit Utilization Below 30%

Now let’s focus on what actually works.

These strategies are simple but highly effective.

1. Pay Before Your Statement Date

Most people wait until the due date to pay—but that’s too late for utilization.

Instead:

- Pay your balance before the statement closes

- This reduces what gets reported to credit bureaus

👉 This is one of the fastest ways to lower utilization instantly.

2. Increase Your Credit Limit

Another powerful method is increasing your available credit.

You can:

- Request a credit limit increase

- Open a new credit card (if responsible)

Example:

- Balance: $2,000

- Limit: $5,000 → 40% utilization

- New limit: $10,000 → 20% utilization

Same spending—better ratio.

3. Use Multiple Credit Cards

Instead of using one card heavily, spread your spending.

- Card A: 20% utilization

- Card B: 15% utilization

This looks much better than one card at 70%.

4. Keep Old Credit Accounts Open

Closing old accounts reduces your total credit limit.

That can increase your utilization—even if your spending doesn’t change.

👉 Longer credit history + higher limits = better score

5. Make Multiple Payments Each Month

You don’t have to wait for one monthly payment.

Try:

- Weekly payments

- Bi-weekly payments

This keeps your balances low at all times.

6. Set Spending Alerts

Many people overspend without realizing it.

Set alerts when you reach:

- 20% usage

- 30% usage

This helps you stay in control.

How Long Does High Credit Utilization Affect Your Score?

Here’s the good news:

Credit utilization has no long-term memory.

It resets every billing cycle.

That means:

- If your utilization is high this month → score may drop

- If you lower it next month → score can recover quickly

However, consistently high utilization will keep dragging your score down.

Credit Utilization Low Meaning (Why Low Is Better)

Low credit utilization shows that:

- You’re not dependent on credit

- You manage debt responsibly

- You have financial discipline

This builds trust with lenders and improves your chances of:

- Loan approvals

- Lower interest rates

- Higher credit limits

To stay financially healthy, learn strategies on how to avoid debt traps.

FAQs: Credit Utilization Ratio Explained

What is a good credit utilization ratio?

A good credit utilization ratio is below 30%, but for the best credit scores, experts recommend keeping it between 1% and 10%.

Is 30% credit utilization too high?

30% is considered the upper safe limit. While it won’t severely damage your score, staying below 10% is ideal for maximum score improvement.

Does credit utilization matter if you pay in full?

Yes, it does. Credit utilization is based on your statement balance, not your payment. Even if you pay in full later, a high reported balance can still affect your score.

How much will lowering credit utilization affect my score?

Lowering utilization can significantly boost your score, especially if you reduce it from high levels (like 70–80%) down to under 30% or 10%.

How to keep credit utilization below 30%?

You can keep utilization low by:

Paying before your statement date

Increasing your credit limit

Using multiple credit cards

Making multiple payments each month

Can 0% utilization hurt your credit score?

Yes, slightly. Having no activity may signal that you’re not using credit. Keeping a small balance (1–10%) is better.

Conclusion

Understanding your credit utilization ratio is one of the simplest yet most powerful ways to take control of your credit score.

While many people focus only on making payments on time, how much of your credit limit you use plays a major role in how lenders evaluate your financial behavior. Even small changes in your utilization ratio can lead to noticeable improvements in your score.

The key takeaway is clear:

Keep your credit utilization below 30%, and ideally under 10% for the best results.

By applying a few smart habits—like paying before your statement date, spreading purchases across multiple cards, and keeping your balances low—you can quickly improve your credit profile without taking on extra debt.

The good news is that credit utilization updates frequently, so positive changes can reflect in your score within a short time.

In the long run, managing your credit utilization wisely not only helps you build a strong credit score but also opens the door to better financial opportunities, lower interest rates, and greater financial stability.

Basic principles of personal finance are essential for improving your credit habits.